The digital lending landscape in India has been undergoing a major transformation. The surge in smartphone penetration, coupled with a growing preference for online financial services, has led to an exponential rise in digital lending platforms. According to the India Digital Lending Report 2023, the digital lending market is expected to surpass ₹12 trillion by 2025, highlighting the increasing demand for seamless, accessible, and efficient lending experiences. However, as the sector grows, so does the need to enhance customer experience to stay competitive. Financial institutions must innovate continuously to meet evolving customer expectations while adhering to regulatory standards. 1. Simplifying the Application Process The intricacy of the loan application procedure is one of the primary causes of consumer discontent with traditional lending systems. Lengthy documentation, numerous verification steps, and opaque procedures frequently deter potential borrowers. By expediting the loan application process, digital lending platforms can greatly enhance the client experience. Artificial intelligence (AI) and machine learning (ML) can help streamline the procedure by automating KYC (Know Your Customer) verification, cutting down on paperwork, and going paperless altogether. Nowadays, many platforms use real-time data, biometric verification, and digital signatures to quickly approve loans and authenticate identities. According to a PwC India report, 70% of consumers prefer to apply for loans online because it takes less time and effort. This change illustrates how crucial it is to streamline and expedite procedures. 2. Personalization through Data Analytics Personalized experiences are no longer a luxury but an expectation. Data analytics plays a crucial role in providing a tailored experience to customers. Lenders can offer personalized loan products that meet individual needs by leveraging customer data—such as spending habits, transaction history, and credit scores. Advanced analytics can also allow lenders to offer dynamic loan amounts and terms based on the borrower’s financial situation. AI-driven recommendations, such as providing customers with loan options that best suit their repayment abilities, can help foster trust and long-term relationships. According to a McKinsey & Company report, personalized financial products increase customer engagement by 80%, as they feel more aligned with their unique needs. 3. Enhancing Speed and Convenience Speed is key to the success of the digital lending market. The ability to get payments quickly is one of the main draws of digital lending platforms. The approval process for loans under traditional lending systems can take days or even weeks. On the other hand, digital platforms can provide loan approvals almost instantly, and the money can be disbursed within a day. Fintech companies are increasingly using sophisticated algorithms that evaluate a borrower’s creditworthiness in real time, allowing for quicker loan approvals and decision-making. With features like round-the-clock accessibility, intuitive user interfaces, and easy navigation, customers now expect a flawless experience. According to Statista, 63% of Indian borrowers actually think that digital lending platforms offer a quicker, more effective experience than traditional banks, according to Statista. 4. Integrating AI for Better Customer Support AI-powered chatbots and virtual assistants have revolutionized customer support in digital lending. These tools can answer queries, provide assistance with loan applications, and guide users through the entire process in real-time. AI-driven customer support is not only faster but also cost-effective, freeing up human agents to address more complex issues. A survey by Accenture found that 63% of customers prefer interacting with AI-powered chatbots for routine inquiries, as they expect quicker and more accurate responses. For digital lending platforms, integrating AI can reduce waiting times, improve service quality, and enhance customer satisfaction. 5. Building Transparency Transparency is key to building trust with customers. Clear communication about loan terms, interest rates, fees, and repayment schedules reduces misunderstandings and dissatisfaction. Many digital lending platforms now outline charges upfront and in simple terms. Offering real-time loan status updates and payment reminders helps customers stay informed. According to the FIS Global Report, 74% of customers prefer lenders with transparent, easy-to-understand terms. 6. Leveraging Digital Payment Solutions Incorporating seamless payment solutions into digital lending platforms enhances customer experience by enabling smooth repayment processes. With the growing adoption of digital wallets, UPI, and other online payment systems in India, borrowers can make quick, hassle-free repayments from their smartphones. Offering flexible payment options, including auto-debit services or pay-as-you-earn models, can improve loan repayment behavior and reduce defaults. Flexible repayment schedules, including variable payment options or the ability to reschedule payments when needed, further enhance customer satisfaction by catering to changing financial circumstances. The Indian digital lending market is exploding, fueled by a surge in demand and a wave of innovative solutions. However, amidst this rapid growth, the customer experience remains the linchpin for success. To truly thrive, lenders must transcend mere convenience and deliver an unforgettable customer journey. This necessitates a radical reimagination of the lending process, from streamlining application procedures to forging unparalleled levels of transparency. Through the power of AI-powered personalization and prioritizing cybersecurity at every touchpoint, lenders can build lasting trust and cultivate a loyal customer base.

Category: Reports and Filings

The Ethical Implications of Gen AI in Fintech in India

India’s fintech sector stands on the brink of a Gen AI-powered revolution, prepared to unlock unprecedented levels of efficiency, innovation, and personalized experiences. However, this transformative potential is inextricably linked to a profound set of ethical dilemmas. The ethical concerns surrounding Gen AI require constant attention, from the threat of algorithmic bias aggravating already-existing inequalities to the constant danger of data breaches. A dedication to ethical AI practices is necessary to navigate this complicated terrain, guaranteeing that innovation advances the common good and creates a genuinely inclusive and equitable financial future for all Indians. 1. Data Governance and Security India’s fintech sector relies on vast amounts of personal and financial data for Gen AI-driven solutions like fraud detection and credit scoring, raising significant privacy concerns. With sensitive data involved, financial institutions must adopt robust data governance frameworks prioritizing privacy. The upcoming Indian Data Protection Bill will guide the sector, ensuring compliance to build trust. Techniques like differential privacy and federated learning can protect sensitive data, while regular audits and transparent data handling practices are essential to safeguard privacy and prevent breaches. 2. Ensuring fairness A key ethical challenge of Gen AI is algorithmic bias. AI systems trained on historical data may reflect societal inequalities, leading to biased outcomes. In India, this could impact credit scoring, disadvantaged groups like women, rural populations, or lower-income communities, furthering financial exclusion. Addressing bias is not just about fairness but also social responsibility. Indian fintech companies must proactively audit models, ensure diverse training data, and use fairness-aware algorithms. Promoting transparency in decision-making and explaining AI outcomes will help build trust and prevent discrimination. 4. Re-skilling for an AI-Driven Economy As Gen AI automates tasks like customer service and transaction monitoring, concerns about job displacement rise, particularly in India’s entry-level financial sector roles. To mitigate this, fintech companies must prioritize reskilling and upskilling initiatives. These programs can help employees transition to higher-value roles, such as AI model monitoring and data analysis, ensuring a workforce that complements AI rather than competing with it. Investing in human capital will help create a future-ready workforce. 5. Ethical Use of AI in Decision-Making Gen AI can influence key financial decisions, such as loan approvals, insurance underwriting, and investment advice. While AI’s ability to analyze vast datasets and identify patterns can improve decision-making accuracy, there is an ethical obligation to ensure these decisions are made responsibly and in the best interest of the customer. Fintechs must implement ethical guidelines that prioritize customer well-being and transparency in AI-driven decisions. This includes ensuring that AI systems are used to empower customers rather than exploit them, such as avoiding over-indebtedness through responsible lending practices. 6. Frameworks for Ethical AI Implementation India’s fintech sector is already operating within a rapidly evolving regulatory environment, with initiatives such as the Reserve Bank of India’s regulatory sandbox and the Indian Data Protection Bill providing a foundation for responsible AI integration. However, there is still a need for clear and comprehensive regulatory frameworks that address the unique challenges posed by Gen AI. The government, in collaboration with industry stakeholders, must develop policies that ensure AI is deployed responsibly across the fintech ecosystem. This includes defining clear standards for data privacy, algorithmic fairness, transparency, and accountability. By aligning regulatory policies with ethical AI principles, India can create a balanced environment that fosters innovation while protecting consumers and ensuring social good. 7. Inclusive Financial Services AI has the potential to drive greater financial inclusion, but only if it is deployed in an inclusive and equitable manner. India’s fintech sector has already made significant strides in providing services to underserved populations, including through digital wallets and micro-lending platforms. However, there is still much work to be done to ensure that AI benefits all segments of society, especially marginalized groups. Fintech companies must design their AI-driven solutions to be inclusive by tackling language barriers, enhancing access to financial services for rural populations, and offering digital literacy programs. By prioritizing inclusivity, India’s fintech industry can ensure that Gen AI does not inadvertently deepen the digital divide but instead fosters a more equitable financial landscape. While the technology holds enormous potential to enhance financial services, it is paramount to understand that it also presents significant risks that must be carefully managed. With the right frameworks in place, India has the opportunity to become a global leader in the ethical integration of AI, driving innovation while safeguarding the interests of consumers and society.

The Impact of Lending on Personal Finance

The emergence of digital lending over the past decade has significantly changed the personal finance landscape. The days of having to go to a bank, fill out a ton of paperwork, stand in line, and wait for your loan to be approved are long gone. These days, thanks to smartphones and technology, you can apply for a loan with a few taps and have it approved faster than you can order a pizza. ember when applying for a loan felt like a month-long waiting game? Well, those days are gone. Digital lending platforms can approve loans in minutes, or even seconds! In India, a country of over 1.4 billion people, digital lending is booming, and the time it takes to get a loan has drastically reduced. According to Statista, the average time to approve a digital loan is now just 15 minutes compared to weeks or even months in traditional banking. The deluge of paperwork that once hampered loan applications has been eliminated by digital financing. Digital lending eliminates the need for paper records. Documents such as bank statements, income certificates, and identification documents can be uploaded straight from your phone. According to PwC, about 70% of Indian borrowers like digital lending because it eliminates the need for documentation. And who was to blame? Instant messaging is like a step up from snail mail! Traditionally, loans were often a privilege for those with an established credit history or a steady job. But digital lending is breaking down these barriers. These platforms are using innovative algorithms and AI to analyze alternative data points, such as utility bills, online shopping habits, and even social media activity, to assess creditworthiness. This means that more people—especially young professionals, students, and those from underserved areas—can access loans they might not have qualified for with traditional banks. NITI Aayog reports that India’s digital lending market is expected to reach ₹12 trillion by 2025, with more people than ever before being able to access financial services. The growth of microloans is one of the most fascinating developments in digital lending. These small loans, which are frequently offered for as little as ₹500 to ₹5,000, are ideal for those who require immediate financial support but do not wish to incur long-term debt. Additionally, microloans are a potent instrument for advancing financial inclusion, particularly for marginalized sector. According to The Economic Times, microloans are currently aiding more than 100 million individuals in India by giving them access to small-scale money for everything from healthcare to education, thereby improving their quality of life. Consider a loan that is customized to your requirements, preferences, and hobbies. Data analytics are being used by digital lenders to customize loan offers. Digital lending platforms are suggesting loan solutions that match your financial profile, just way Netflix suggests movies based on your viewing history. For instance, you can be given a loan with better terms or cheaper interest rates if you regularly pay your payments on time. According to McKinsey & Company, 80% of consumers want individualized financial products, and digital lending is well-positioned to provide this experience. Digital lending platforms assist with debt management in addition to providing loans. The dashboards on the majority of platforms are easy to use, allowing borrowers to monitor loan disbursements, repayments, and even determine their cumulative interest payments. The real fun happens when these platforms use AI to assist users in creating customized payback plans that adapt to their financial circumstances. It’s like having a personal money assistant on call all the time. The rise of Buy Now, Pay Later (BNPL) schemes is one of the most exciting trends in digital lending. BNPL allows consumers to make purchases and pay in installments, often interest-free if repaid quickly. It’s especially popular for shopping, travel, and education. A Bain & Company report predicts BNPL in India will grow 4-5 times in the coming years, transforming how consumers manage small debts. With fintech innovations, the future of personal finance is brighter, smarter, and more inclusive than ever before. So next time you need a quick loan, remember: the future of borrowing is just a click away!

Building Trust in Gen AI: A Roadmap for the Financial Industry

Generative AI is rapidly emerging as a transformative force in the financial industry, with the potential to revolutionize operations, enhance efficiency, and deliver tailored experiences to customers. From automating tasks to improving fraud detection and predictive analytics, Gen AI holds great promise. However, its successful integration into the financial sector depends heavily on building trust among stakeholders, including regulators, institutions, employees, and customers. Key Challenges and Considerations As Indian financial institutions explore the potential of Gen AI, several key challenges must be addressed to build trust and ensure its effective integration: Safeguarding sensitive customer data is paramount, and establishing robust data governance frameworks is essential for privacy protection and compliance with regulations like the Indian Data Protection Act. This builds trust, ensuring that data is handled securely. AI models can inherit biases from training data, leading to unfair outcomes. Proactive bias detection and mitigation are crucial to ensure that AI systems produce fair and equitable results, fostering trust among users. Additionally, many AI models are “black boxes,” making it difficult to understand how decisions are made. Investing in explainable AI (XAI) techniques is vital to provide transparency and accountability, allowing users to comprehend and trust AI-driven decisions. AI-driven automation also raises concerns about job displacement. To address this, financial institutions should focus on reskilling and upskilling employees, ensuring a smooth transition to an AI-enhanced future. Finally, establishing ethical guidelines and responsible AI practices is critical. Ensuring AI aligns with societal values and accountability will help institutions deploy the technology in a responsible manner that benefits both businesses and society. Building a Trustworthy Gen AI Ecosystem To successfully integrate Gen AI into finance, institutions must focus on several key actions to create a trustworthy ecosystem. The Indian Fintech Landscape India’s fintech sector has emerged as one of the fastest-growing globally, driven by a young and tech-savvy population, widespread smartphone usage, and a regulatory environment that supports innovation. AI adoption in the Indian fintech sector is accelerating, with companies leveraging machine learning, natural language processing, and computer vision to enhance customer experience, improve fraud detection, and automate financial processes. However, challenges persist, including limited access to financial services for underserved populations, cybersecurity threats, and the need for enhanced financial literacy. The Reserve Bank of India (RBI) has been proactive in encouraging the responsible use of AI, with a focus on data privacy, security, and fairness. The Indian regulatory framework provides a foundation for responsible AI adoption, making it an ideal environment for building a trustworthy Gen AI ecosystem. India’s rapidly growing fintech sector, supported by a forward-thinking regulatory environment, is well-positioned to lead the world in the ethical and responsible adoption of Gen AI. By nurturing a collaborative ecosystem emphasizing human-centric AI and accountable innovation, India’s financial institutions must exercise the transformative power of Gen AI to reshape the future of finance, delivering a more inclusive, efficient, and personalized financial experience for all.

The Future of Digital Lending: Emerging Technologies and Innovations in India

Digital lending has fundamentally transformed the way financial institutions and borrowers engage in India. Fueled by the widespread adoption of smartphones, increased internet connectivity, and supportive government initiatives aimed at fostering digital financial inclusion, the digital lending sector has experienced remarkable growth. This shift has not only made access to credit more convenient and efficient but has also empowered underserved populations by bridging the gap between traditional banking services and emerging digital solutions. As a result, digital lending is reshaping the financial ecosystem, providing greater financial accessibility to millions of Indians. Current State of Digital Lending in India According to a report by Redseer Strategy Consultants, digital lending in India is projected to account for 5% of all retail loans by FY28, up from 1.8% in FY22. The key drivers of its growth include increasing smartphone penetration, government initiatives like Digital India and UPI, and rising demand for credit among the middle class and underserved segments. A diverse range of players, including banks, NBFCs, and fintech companies, are actively participating in the digital lending space. Emerging Technologies and Innovations Challenges, opportunities and the way forward Despite challenges, digital lending has a bright future in India. By embracing emerging technologies and addressing regulatory concerns, the industry can explore its full potential, driving financial inclusion and significantly contributing to the country’s economic growth. These challenges include ensuring data privacy and security, the establishment of a clear and supportive regulatory framework to foster innovation while protecting consumer interests, and improving financial literacy among borrowers to help them make informed borrowing and repayment decisions. The future of digital lending in India holds immense promise, fueled by these emerging technologies. These innovations are revolutionizing the lending ecosystem, enhancing efficiency, security, and customer experience. By overcoming existing challenges and capitalizing on new opportunities, India is poised to become a global leader in digital lending. This transformation will not only drive financial inclusion but also empower millions of citizens, creating a more accessible and equitable financial landscape for all.

Embedded Finance in the Indian Fintech Sector

India’s fintech sector has been one of the key drivers behind the rise of embedded finance. With its massive population, diverse financial needs, and high mobile penetration, India is an ideal market for this transformation. The combination of government support, digital infrastructure which aims to provide financial services to underserved communities, and the proliferation of smartphones has created an environment ripe for the growth of embedded finance. However, the opportunities are vast. As mobile penetration increases and fintech adoption continues to rise, embedded finance can play a crucial role in accelerating financial inclusion, especially among India’s large unbanked and underbanked populations. By providing easy access to essential financial products, India’s fintech sector can unlock new economic opportunities for millions. Conclusion The rise of embedded finance represents a paradigm shift in how financial services are delivered and consumed. With its seamless integration into everyday platforms, it offers convenience, personalization, and greater financial inclusion. India’s fintech sector, with its rapidly advancing digital infrastructure, is well-positioned to capitalize on the opportunities offered by embedded finance, ultimately transforming the financial landscape for millions of citizens. As the sector continues to evolve, it will be crucial for businesses, regulators, and consumers to collaborate in overcoming challenges, safeguarding security, and unlocking the full potential of this transformative trend.

How Gen AI is Revolutionizing Customer Experience in Fintech

Generative AI is rapidly reshaping industries, and fintech is no exception. By utilizing the power of AI, fintech companies are redefining customer experiences, making financial services more accessible, personalized, and efficient. Personalized Financial Advice One of the most significant impacts of Gen AI on fintech is the ability to provide highly personalized financial advice. AI-powered chatbots and virtual assistants can analyze vast amounts of data, including transaction history, spending patterns, and risk tolerance, to offer tailored recommendations. For instance, a chatbot can suggest investment opportunities aligned with a user’s financial goals or recommend budgeting strategies to optimize cash flow. A recent study by Capgemini found that 71% of consumers are willing to share their financial data with AI-powered tools in exchange for personalized advice. This growing trust in AI-driven solutions underscores the potential for Gen AI to revolutionize financial planning and advisory services. Enhanced Customer Support Gen AI-powered chatbots and virtual assistants are transforming customer support in the fintech industry. These AI-driven tools can handle a wide range of inquiries, from simple account balance checks to complex troubleshooting. By automating routine tasks, these tools free up human agents to focus on more complex issues, improving overall customer satisfaction. Moreover, AI can analyze customer sentiment in real-time, allowing businesses to identify and address potential issues proactively. This proactive approach can significantly reduce customer frustration and churn. Fraud Detection and Prevention Fraudulent activities pose a significant threat to the fintech industry. Gen AI can play a crucial role in detecting and preventing fraud by analyzing vast amounts of transaction data in real-time. AI algorithms can identify anomalies and suspicious patterns that may indicate fraudulent activity, enabling financial institutions to take swift action to protect their customers. A study by Juniper Research estimates that AI-powered fraud prevention solutions could save the financial services industry $8 billion by 2026. Seamless User Experiences Generative AI is revolutionizing the fintech industry by enabling companies to deliver seamless, intuitive, and highly personalized user experiences. For instance, AI-powered voice assistants allow users to effortlessly interact with their financial accounts using natural language, streamlining the process of managing finances on the go. Moreover, AI-driven personalization tailors the user interface to individual preferences, offering customized recommendations and services that significantly enhance user engagement and satisfaction. By leveraging these advanced AI technologies, fintech companies are not only improving convenience but also creating a more dynamic and user-centric financial environment. The Future of Fintech As generative AI continues to evolve, its transformative impact on the fintech industry is poised to expand significantly. By embracing this technology, fintech companies can unlock exciting new opportunities, enhance customer experiences, and gain a substantial competitive advantage. While it’s important to address ethical considerations and ensure responsible and transparent AI usage, the potential for growth is immense. With the power of AI, fintech companies can build deeper, more meaningful relationships with their customers, foster trust, and drive sustained long-term success.

The Future of Fintech: How Gen AI is Reshaping the Industry

Generative Artificial Intelligence or Gen AI as we call it is rapidly reshaping the fintech landscape, offering significant advancements that are transforming financial services across the globe. As AI models become more advanced, they are driving the next generation of fintech innovations, improving customer experiences, optimizing operational efficiency, and enhancing security protocols. By analyzing vast amounts of data and automating complex processes, Gen AI is poised to redefine the way financial institutions and fintech companies interact with customers and make strategic decisions. 1. Personalized Financial Advice Gen AI leverages vast data sets, including spending habits, income, and economic trends, to deliver highly personalized financial advice, such as customized investment strategies, retirement planning, and budgeting solutions. It can also forecast market movements and recommend adaptive strategies, helping clients make informed decisions. Furthermore, AI-powered virtual assistants and chatbots provide real-time, 24/7 customer support, delivering tailored responses, resolving specific concerns, and offering proactive guidance. This enhances customer satisfaction by ensuring fast, accurate, and accessible service at any time, creating a seamless and personalized experience. 2. Automated Financial Processes AI-driven automation is transforming back-office operations within the fintech industry by streamlining tasks that were traditionally time-consuming and manual. Processes like loan processing, fraud detection, and compliance checks are now being automated, enabling financial institutions to operate more efficiently and accurately. AI can analyze vast and complex data sets in real-time, identifying patterns and anomalies that human teams might miss, thus enhancing decision-making and reducing the risk of errors. This capability extends to optimizing risk management by assessing creditworthiness, predicting potential risks, and fine-tuning investment strategies with greater precision. The result is a more efficient operation that reduces costs, improves regulatory compliance, and delivers better financial outcomes for both institutions and customers. By leveraging AI, fintech companies can enhance their service offerings, respond faster to market changes, and provide more personalized, data-driven financial solutions. 3. Enhanced Security and Fraud Prevention AI is revolutionizing fintech by bolstering security and fraud prevention. By analyzing vast amounts of transaction data in real-time, AI can swiftly identify anomalies and suspicious patterns, enabling swift action to thwart fraudulent activities. This proactive approach significantly reduces financial losses and builds trust between financial institutions and their customers. Furthermore, AI acts as a vigilant guardian of sensitive financial information. By continuously monitoring networks and systems, AI can proactively identify vulnerabilities, predict potential attacks, and deploy countermeasures before damage occurs. 4. Innovative Financial Products AI is driving the evolution of fintech by enabling the creation of personalized financial products and innovative business models. From tailored insurance policies and investment portfolios to predictive analytics for risk assessment and AI-powered trading platforms, Gen AI is reshaping the financial landscape, delivering more relevant and efficient solutions. The Road Ahead The future of fintech powered by Gen AI looks promising. As AI technologies continue to evolve, they will become even more integrated into financial services, driving innovation, efficiency, and customer satisfaction. Financial institutions and fintech companies that embrace AI will be better equipped to meet the demands of an increasingly digital, data-driven world. However, the challenges associated with AI adoption—particularly in the areas of data privacy, ethics, and regulation—must be carefully managed to ensure that the benefits of this technology can be fully realized. By addressing these concerns, the fintech industry can build a more efficient, inclusive, and customer-centric future for financial services. As we look to the future, the full potential of AI in reshaping the financial landscape will continue to unfold, ushering in an era of smarter, more personalized, and more efficient financial services.

How Digital Platforms Are Revolutionizing Credit Access

The digital revolution has irrevocably reshaped industries worldwide, and the credit sector is no exception. Technological advancements are propelling a paradigm shift in how individuals and businesses access financial resources. With unprecedented speed, convenience, and inclusivity, digital platforms are democratizing credit, making it more accessible to a broader range of borrowers. Expanded Access to Credit One of the most significant impacts of digital platforms is the expansion of credit access. Traditionally, obtaining credit often required navigating cumbersome paperwork and dealing with lengthy approval processes. Digital platforms, however, streamline these processes, allowing users to apply for and receive credit with just a few clicks. According to a 2023 report by the World Bank, digital lending platforms have increased credit access by 20% in emerging markets, where traditional banking infrastructure is often limited. Enhanced Inclusivity Digital platforms are also breaking down barriers to credit for underserved populations. Fintech companies leverage alternative data—such as payment histories from utilities and telecommunications—to assess creditworthiness, making it easier for individuals without traditional credit histories to access loans. This approach has proven effective; a study by the McKinsey Global Institute found that alternative data usage in credit scoring has led to a 25% increase in loan approvals for individuals from low-income backgrounds. Efficiency and Speed The efficiency and speed of digital credit platforms surpass traditional methods. Automated systems and artificial intelligence (AI) allow for rapid processing of applications and real-time credit scoring. A recent survey by PwC revealed that 65% of borrowers on digital lending platforms reported receiving their funds within 24 hours of application approval, compared to an average of 10-15 business days through traditional banks. This rapid turnaround is particularly beneficial for small businesses and individuals facing urgent financial needs. Personalization and Customer Experience Digital platforms enhance the borrower experience through personalized services. AI-driven algorithms analyze user behavior and preferences to offer tailored credit products and recommendations. This personalization improves user satisfaction and helps borrowers find products that best suit their needs. According to a report by Accenture, 70% of users on digital lending platforms reported higher satisfaction levels due to the personalized nature of the services they received. Data Security and Privacy Despite these advancements, digital platforms must address concerns around data security and privacy. With the increased reliance on personal and financial data, safeguarding this information becomes crucial. Leading platforms invest in advanced encryption technologies and adhere to stringent regulatory standards to protect user data. For instance, the European Union’s General Data Protection Regulation (GDPR) has set a high standard for data privacy, and compliance with such regulations is becoming a norm for global digital credit platforms. Future Outlook Looking ahead, digital platforms are expected to continue driving innovation in credit access. Advances in technologies such as blockchain and biometric authentication promise to further enhance security and streamline processes. As digital platforms evolve, they will likely offer even more inclusive and efficient solutions, making credit accessible to an increasingly broad audience.

Fintechs and small finance banks – Competition or Collaboration?

The financial landscape is undergoing a rapid transformation, driven by technological advancements and evolving customer expectations. At the heart of this disruption are fintechs, with their innovative solutions and agile approach, and small finance banks, striving to bridge the financial inclusion gap. This dynamic interplay raises a critical question: are these two forces destined to be competitors or collaborators? The intricate relationship between fintechs and small finance banks explores the potential synergies and challenges that shape their coexistence. Alignment and Shared Vision In today’s fast-paced era of digital banking, small finance banks aim to modernize banking through technology by aligning perfectly with fintechs’ commitment to financial innovation. This partnership leverages the strengths of both institutions, offering a wider range of accessible financial products and services through Fintech’s extensive distribution network. Enhanced Products and Convenience The usual product suite of small finance banks includes savings and current accounts with competitive rates and flexible features which could become conveniently available through a mobile app of any fintech company. This eliminates the need for physical visits to branches. A fintech’s secure payment infrastructure further strengthens the user experience. The collaboration between the two will empower aspiring entrepreneurs by providing financial support, flexibility, and expertise to grow their businesses. A 2024 report by the Reserve Bank of India highlighted that transactions through digital channels have seen a year-on-year increase of 30%, largely attributed to collaborations between SFBs and fintech firms. This surge reflects the growing integration of technology in banking services. Competition Fosters Innovation The rise of fintechs has challenged the traditional banking landscape, including SFBs. Fintechs often offer more convenient and affordable financial solutions, attracting customers away from established institutions. SFBs are caught between traditional banks and fintechs, particularly in the digital space. They must adapt quickly to compete effectively. This competition can drive positive change, pushing SFBs to invest in technology, improve customer experience, and explore new business models. The relationship between fintechs and SFBs is multifaceted. While they compete in some areas, collaboration offers significant potential benefits for both parties and, ultimately, consumers. Building Successful Collaboration Strategic partnerships require trust, clear communication, and a shared vision for financial inclusion and innovation. Supportive regulations and policies are crucial for fostering collaboration and a fair playing field. The NASSCOM Fintech Report 2024 stated that SFBs have significantly increased their investment in fintech solutions, with a 40% rise in funding allocated to fintech startups compared to the previous year. This investment is focused on areas such as digital lending, payments, and customer engagement. A Journey, Not a Rivalry The dynamic between Fintechs and SFBs is far from a zero-sum game. Instead of viewing each other as competitors, both sectors have the opportunity to thrive through collaboration and constructive competition. By joining forces and leveraging their unique strengths, fintechs and SFBs can drive meaningful advancements in financial services, enhance access for diverse populations, and uncover new pathways for mutual growth and prosperity. This partnership promises not only to reshape the financial landscape but also to foster an environment where innovation and inclusivity flourish together.

Innovative financing models for MSMEs beyond Traditional banking

Traditional banks have long been the go-to source of funding for MSMEs. However, for many securing a loan from a bank can be a frustrating and time-consuming process, often hindered by stringent collateral requirements and lengthy approval times. This limited access to capital can stifle growth and innovation, hindering the immense potential of the MSME sector. The financial landscape is evolving, and a wave of innovative financing models is emerging specifically to address the financing needs of MSMEs. Peer-to-peer (P2P) lending – This platform allows borrowers to connect directly with individual lenders via online platforms. It eliminates the intermediary, which lowers costs and increases MSMEs’ access to capital. According to Industry ARC, the India P2P lending market size is expected to reach $10.5 billion by 2026. Besides P2P, crowdfunding has become a favoured method for MSMEs to secure capital. One notable trend in the Indian crowdfunding market is the emergence of specialized platforms tailored to specific industries or causes. These platforms focus on supporting startups, social enterprises, and creative endeavors, reflecting the diverse interests and needs of Indian consumers. This trend underscores the growing acceptance of crowdfunding as a viable alternative to traditional funding avenues. Invoice financing – This model helps businesses manage cash flow issues without waiting for customers to pay their invoices. Firstly, it provides immediate access to cash flow by allowing businesses to obtain advances against their outstanding invoices, addressing liquidity challenges, and enabling timely payments of operational expenses. Secondly, it eliminates the need to wait for customers to settle invoices, thereby accelerating the cash conversion cycle and enhancing working capital management. Additionally, invoice financing does not add to the company’s debt burden, as it is not considered a loan, making it an attractive option for businesses seeking non-dilutive financing. Overall, invoice financing enables MSMEs to maintain steady cash flow, improve financial stability, and seize growth opportunities more effectively. Industry estimates suggest that the invoice discounting ecosystem in the country per month is about Rs 1 lakh crore. Supply Chain Financing – Supply chain financing (SCF) involves optimizing the flow of capital across the supply chain. Financial institutions and fintech firms offer SCF solutions such as reverse factoring, dynamic discounting, and trade credit. According to the Global Supply Chain Finance Forum, the SCF market could reach $2.7 trillion by 2025. SCF benefits include improved liquidity, lower financing costs and strengthened relationships through collaboration between buyers and suppliers. Innovative financing models are transforming the landscape for MSMEs, offering alternatives to traditional banking that are more accessible, flexible, and tailored to their needs. As these models continue to evolve and gain traction, they hold the potential to bridge the financing gap and drive sustainable growth for MSMEs worldwide. Policymakers, investors, and financial institutions must continue to support and promote these innovative solutions to foster a more inclusive and dynamic economy.

Role of AI in Supply Chain Finance Management

India’s supply chain, an essential component of its quickly developing economy, is presently going through a significant digital revolution. Artificial Intelligence, which is drastically changing the field of supply chain finance, is leading this transformation. India is leading the way in creating a more inventive and robust financial ecosystem within its supply chains by utilizing AI to increase operational efficiencies. AI in Supply Chain Finance Artificial Intelligence is revolutionizing Supply Chain Finance (SCF) in India by using its capability to process vast volumes of data with unparalleled speed and precision. Here’s how AI is transforming the landscape: Credit Risk Assessment: AI-powered algorithms are redefining credit risk evaluation by analyzing extensive financial data, payment histories, and market trends. This enhanced analytical capability allows for more accurate and efficient assessments of creditworthiness, facilitating quicker decision-making and minimizing risk for lenders. Fraud Detection: AI excels in identifying anomalies within transaction patterns, serving as a robust defense against fraudulent activities. By detecting irregularities early, AI safeguards both lenders and borrowers from potential financial losses and ensures greater security in financial transactions. Invoice Processing: AI-driven optical character recognition (OCR) technology automates the extraction of data from invoices, significantly reducing manual input and minimizing errors. This streamlines the invoicing process, enhances accuracy, and accelerates payment cycles. Predictive Analytics: With its advanced predictive capabilities, AI can forecast cash flow, demand patterns, and potential supply chain disruptions. This foresight enables businesses to make proactive decisions, optimize working capital, and better prepare for future challenges. Supply Chain Optimization: AI identifies and addresses inefficiencies within the supply chain, such as inventory mismatches or transportation delays. By offering actionable insights and recommendations, AI helps businesses reduce costs, enhance operational efficiency, and achieve a more streamlined supply chain. In summary, AI’s integration into supply chain finance not only enhances accuracy and efficiency but also provides a strategic advantage in navigating the complexities of modern financial operations. Impact on Indian supply chain finance While the full potential of AI in India’s SCF is yet to be realized, early indicators are promising. A study by McKinsey Global Institute estimates that AI could add up to $1 trillion to India’s GDP by 2030. While specific data on the impact of AI on SCF in India is limited, the broader trend of digital transformation and the increasing adoption of AI across sectors suggest a significant positive impact. Despite the immense potential, challenges such as data quality, infrastructure, and regulatory hurdles need to be addressed for widespread AI adoption in SCF. However, the opportunities for innovation and growth are significant. AI has the potential to revolutionize supply chain finance in India by improving efficiency, reducing costs, and mitigating risks. As the technology matures and becomes more accessible, we can expect to see even more groundbreaking applications in this space.

The Impact of BNPL on Consumer Behavior and Financial Markets in India

The advent of Buy Now, Pay Later services has revolutionized consumer behavior and financial markets in India, marking a paradigm shift in how individuals and businesses engage with credit and commerce. This innovative financial tool has rapidly gained traction, driven by the increasing digitalization of the economy and a burgeoning preference for seamless, cashless transactions. By democratizing access to credit, BNPL has not only transformed spending habits across various demographics but has also played a pivotal role in enhancing financial inclusion. Transformation of Consumer Behavior BNPL services have significantly increased Indian consumers’ purchasing power by providing flexible payment options that reduce the financial burden of immediate expenses. The Indian BNPL market is expected to grow at a CAGR of more than 45%, reaching USD 45-50 billion by 2026. It has also significantly accelerated e-commerce growth in India, transforming consumer purchasing behavior. Major e-commerce platforms, such as Amazon and Flipkart, have included BNPL options, making high-value items more accessible to a wider audience. These services not only improve customer convenience, but they also increase average order values, contributing to India’s overall e-commerce growth. The BNPL services have profoundly transformed spending patterns and bolstered financial inclusion in India. This rapid adoption has been driven by increasing digitalization and a growing preference for cashless transactions, especially among the younger population. BNPL services have democratized access to credit, with many prominent fintech platforms enabling consumers to make purchases without immediate full payment, thereby facilitating smoother cash flow management. Notably, BNPL transactions have surged across sectors such as e-commerce, travel, and healthcare, with e-commerce witnessing a 55% increase in transaction volume in 2023. This growth has been crucial in extending financial services to underserved segments, as BNPL platforms typically feature simpler onboarding processes and lower credit barriers compared to traditional credit systems. For instance, in rural areas, BNPL has empowered small business owners and consumers to access essential goods and services, thereby fostering economic participation and growth. Implications for Financial Markets While BNPL presents significant growth opportunities, it also introduces risks, particularly related to credit defaults. The ease of access to BNPL services can lead to over-borrowing, especially among consumers who may not fully grasp the implications of deferred payments. This has raised concerns among regulators about the potential for increased debt levels and financial instability. The Reserve Bank of India has acknowledged these risks and is contemplating regulatory measures to ensure responsible lending practices. Implementing guidelines and oversight will be crucial in maintaining a balance between fostering innovation and protecting consumers. BNPL is revolutionizing traditional lending models by providing an attractive alternative to credit cards and personal loans. This disruption is compelling banks and other financial institutions to adapt their offerings to stay competitive. As a result, many are now partnering with BNPL providers or creating their own installment-based products to capture a share of this rapidly expanding market. The integration of BNPL solutions into their portfolios is not only a strategic response to changing consumer preferences but also a proactive measure to retain customer loyalty and drive growth in an evolving financial landscape. By and large, the future of BNPL in India will depend on how well the challenges are managed and how effectively the sector adapts to regulatory developments. As BNPL continues to evolve, it holds the potential to redefine the financial landscape, driving economic growth and improving the lives of millions of Indian consumers.

What is Decentralized Finance (DeFi) and how does it work?

Decentralized finance, or DeFi, isn’t just a tweak to the financial system; it’s a seismic shift shaking the very foundations of traditional finance. Imagine a world where financial transactions are not governed by banks or brokerage firms but instead are transparent, accessible, and autonomous. DeFi makes this vision a reality by implementing the power of blockchain technology, creating a borderless financial playground where individuals have full control over their assets. No longer bound by intermediaries, people can dive into a plethora of financial activities, from lending to trading, without needing anyone’s permission. This liberation not only democratizes finance but also sparks a wave of innovation, giving rise to a dazzling array of decentralized applications (dApps) that cater to diverse financial needs. With DeFi, the promise of inclusivity and efficiency is within reach, heralding a new era where anyone, anywhere, can engage in a truly global and decentralized financial system. Application and Usage DeFi leverages advancements in software, hardware, connectivity, security protocols, and peer-to-peer financial networks. Banks and other financial service providers are eliminated by this system. These businesses charge both consumers and businesses for the use of their services, which are essential to the functioning of the current system. By utilizing blockchain technology, such as Ethereum and Binance Smart Chain ecosystem, DeFi can lessen the requirement for these middlemen. Secondly, DeFi platforms are interconnected through standardized protocols and interoperable interfaces, allowing users to seamlessly navigate between different applications and services. This interoperability fosters innovation and liquidity within the DeFi ecosystem. Many DeFi platforms also embrace community-driven governance models, empowering users to participate in protocol decision-making and vote on proposed changes or upgrades. This decentralized governance ensures transparency, accountability, and resilience against centralized control or manipulation. Roadmap and Growth Opportunities The Indian government’s push towards a cashless economy presents significant growth opportunities. The recent approval of the First Loss Default Guarantee (FLDG) underscores the effectiveness of the bank-fintech partnership model in digital lending. According to Statista, the number of users in the Indian DeFi market is expected to reach 6.26 million by the year 2028. This rapid growth underscores the increasing acceptance and integration of DeFi into mainstream financial systems. Globally, the total value locked (TVL) in DeFi protocols has skyrocketed, reaching over $100 billion in 2023, a testament to the sector’s explosive growth. As decentralized finance continues gaining momentum, its potential to redefine the fabric of global finance becomes increasingly evident. Each day, more individuals join this groundbreaking movement, contributing to its growth and evolution. The journey towards a truly decentralized financial system is not without challenges, but the rewards are immense. As we look ahead, the possibilities are boundless, with DeFi poised to democratize access to financial services, drive innovation, and empower individuals worldwide.

Challenges and Opportunities for NBFCs in India

A potentially rich environment of opportunities and challenges arises in the complex world of NBFCs in India. Functioning as essential elements of the country’s financial system, NBFCs are at the intersection of innovation, risk, and socioeconomic dynamics, ready to spark development and wealth. But they face a host of challenges in the face of rapidly evolving regulations, technological advancements, and macroeconomic swings, from liquidity issues to governance conundrums. However, behind these obstacles are opportunities for them to rethink their mission, embrace flexibility, and develop inclusive financial solutions that go beyond conventional norms. This prompts a profound inquiry: how can NBFCs navigate the uncertain path ahead, utilizing adversity as a catalyst for innovation, and forging a trajectory where challenges evolve into stepping stones towards enduring success? Challenges for NBFCs in India 1. Keeping up with the Regulations – NBFCs in India operate within a rigorous regulatory framework established by the Reserve Bank of India. While these regulations are essential for safeguarding financial stability, they can be seen as constraining by NBFCs. Moreover, changes in regulatory policies or the introduction of new guidelines often necessitate swift adaptation, requiring NBFCs to invest in technology and enhance their compliance infrastructure. The intricate and dynamic nature of these regulations necessitates continuous vigilance and proactive measures from NBFCs, influencing their strategic planning and resource allocation decisions. 2. Funding and Liquidity Management – NBFCs heavily rely on external funding for their lending activities, unlike traditional banks that utilize customer deposits. They depend primarily on borrowing from banks, issuing bonds, or obtaining loans from financial institutions. Securing sufficient funding can be especially challenging during economic downturns or periods of financial instability, leading to higher borrowing costs and restricted access to credit. This directly impacts their liquidity and ability to expand operations. Effective liquidity management is crucial for NBFCs to meet financial obligations such as loan repayments and regulatory compliance. Balancing various funding sources, managing liquidity effectively, and sustaining profitability are ongoing challenges for NBFCs in India. Opportunities for NBFCs 1. Explore Niche Markets – NBFCs can succeed by discovering and targeting specific markets. This could include sectors such as microfinance, where small loans are provided to individuals or businesses who typically lack access to traditional banking services. For this, NBFCs may offer small loans with flexible repayment terms to support the financial needs of entrepreneurs and small businesses. NBFCs can concentrate their resources and efforts on developing expertise in particular industries by concentrating on those. This would include investing in staff training, creating customized underwriting models, and establishing partnerships with stakeholders in the sector. 2. Co-lending opportunities – Collaboration with banks through co-lending arrangements, as approved by the RBI, can be a win-win situation. By working together to increase liquidity, NBFCs can expand their lending portfolios without overburdening their balance sheets. Additionally, co-lending agreements allow the parties to share risks, reducing individual exposure and increasing portfolio diversification. These partnerships give NBFCs access to a steady stream of funding and opportunities for strategic expansion and market share. Co-lending agreements, taken as a whole, enable NBFCs to maximize lending operations, cultivate resilience, and seize new opportunities in the ever-changing financial landscape. 3. Digital Transformation – NBFCs use data analytics to make well-informed decisions rapidly and accurately, ranging from the digitization of loan origination and underwriting processes to the integration of AI-powered credit scoring models. Additionally, they are revolutionizing customer engagement through digital channels such as mobile apps and online platforms, providing seamless experiences for tasks like account management, payments, and support services. They are also strengthening cybersecurity measures to protect sensitive information and transactions, thereby fostering trust and reliability amongst users in the digital domain. NBFCs in India find themselves at a critical juncture, grappling with regulatory challenges and fierce market competition while also being presented with promising avenues for growth. In navigating this landscape, it becomes imperative to foster robust coordination and engagement among regulators, fintech enterprises, traditional financial institutions, and other relevant stakeholders.

The Impact of Open Banking on consumer finance

Open banking is reshaping the financial landscape by revolutionizing how consumers interact with their banks and financial services. Greater openness, competition, and innovation are being promoted by this revolutionary approach to banking, which resulted from changes in regulations and technical breakthroughs. Open banking is fostering the development of a more vibrant and diverse financial ecosystem by permitting third-party providers to access financial data with consumer authorization. Increased Openness in Finance The rise in financial transparency is one of open banking’s most important effects. Because they can now have a more complete picture of their financial information, consumers are better equipped to make judgements. A survey published by Accenture states that new financial services enabled by open banking are of interest to 57% of worldwide consumers. This transparency also extends to more efficient comparison of financial goods and services, since open banking platforms frequently compile information from various accounts to present a cohesive picture of one’s financial situation. Increased Innovation and Competition By enabling new fintech businesses and third-party suppliers to enter the market, open banking promotes competition. As a result of the increased competition, innovative financial products and services that are suited to the demands of customers are developed. According to research by the UK’s Financial Conduct Authority (FCA), the number of fintech businesses entering the market increased by 30% after open banking policies were put into place. Personalized financial management tools, improved credit score algorithms, and creative payment methods are some of these advancements. Enhanced Credit Accessibility Through the provision of more thorough and accurate financial information to lenders, open banking greatly improves consumers’ access to credit. Customary credit scoring algorithms frequently depend on sparse data, which may omit people with weak credit histories. More data, such as transaction histories and spending habits, are available to lenders through open banking, which helps them create more precise credit evaluations. According to a Deloitte research, the use of open banking by 60% of lenders resulted in better credit risk assessments and lower loan default rates. Enhanced Security and Consumer Control Robust safeguards are established to protect customer data, ensuring that security and control remain top priorities in open banking. Regulations such as the UK’s Open Banking Initiative and the EU’s PSD2 (Payment Services Directive 2) enforce stringent data security standards. Consumers have the autonomy to select which third-party providers can access their data and can revoke this access at any time. According to a survey by the Open Banking Implementation Entity (OBIE), 87% of consumers feel confident about the security of their data within open banking environments. Challenges and Future Outlook While open banking offers numerous benefits, it also presents challenges, including data privacy concerns and the need for robust cybersecurity measures. As the open banking ecosystem evolves, ongoing efforts are required to address these issues and ensure a secure and equitable financial environment. Looking ahead, the impact of open banking is expected to grow, with more countries adopting similar regulatory frameworks and technological advancements.

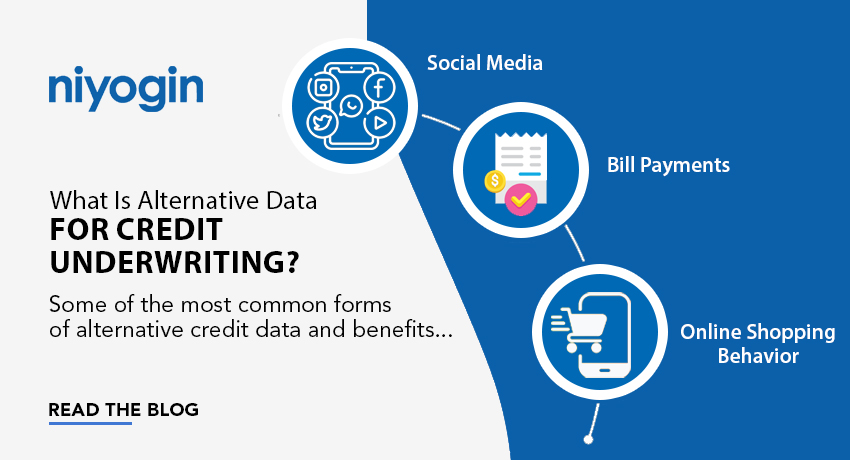

Credit Scoring and Risk Assessment in Digital Lending

Technology’s increasing pervasiveness and the growing call for financial inclusion are driving a rapid transformation of the Indian lending sector. The crucial roles of credit scoring and risk assessment are at the center of this evolution. After relying primarily on credit bureau data for a long time, the industry is now adopting a new paradigm that includes advanced analytics and alternative data sources in order to better assess borrowers. This shift is driven by several factors, including: From Traditional to Transformative A pivotal shift is underway, marked by the increased adoption of alternative data sources such as mobile phone usage, social media activity, and utility bill payments. These data, combined with the power of advanced analytics and machine learning, are enabling the development of more sophisticated credit scoring models that can accurately assess the creditworthiness of a broader population, including those with limited credit history. Regulatory initiatives like the RBI’s regulatory sandbox are fostering innovation by providing a controlled environment for lenders to experiment with new technologies and data sources. Moreover, the rise of open banking is facilitating the seamless sharing of customer data between banks and fintech companies, enriching the data pool available for credit assessment and ultimately enhancing the overall lending ecosystem. These trends are expected to make credit scoring and risk assessment in India more accurate, efficient, and inclusive. This will not only benefit lenders by reducing their risk of bad loans but also benefit borrowers by making it easier for them to access credit. As the industry continues to evolve, it is imperative to strike a balance between innovation and responsible lending. Robust data privacy and security measures, coupled with ethical considerations, will be paramount in building a sustainable and trustworthy credit ecosystem. The future of lending lies in the intelligent and responsible utilization of data to empower both borrowers and lenders.

How do Robo-advisors in the fintech landscape use AI algorithms?

Robo-advisors are revolutionizing the rapidly evolving fintech landscape by employing AI and Gen AI algorithms to deliver tailored financial guidance to investors. These automated investment platforms utilize sophisticated algorithms and machine learning techniques to assess risk profiles, analyze data, and craft personalized investment strategies that align with each client’s unique objectives and preferences. Unlike traditional financial advisors, robo-advisors leverage AI algorithms to gather and process data on investors’ goals, risk appetite, and financial circumstances, leveraging this information to propose customized investment portfolios. Artificial Intelligence Algorithms Driving Personalization Robo-advisors aid in data aggregation and analysis by collecting information from a variety of sources, such as risk profiles, investment preferences, and financial accounts. Through the processing of this data, AI algorithms can generate customized investment recommendations by gaining insight into the financial situations, goals, and risk appetite of investors. AI systems also help evaluate the risk profiles of investors by looking at variables like age, income, time horizon for investments, and risk appetite. Robo-advisors have fundamentally transformed wealth management by democratizing access to advanced investment strategies that were once limited to affluent investors. Their automated, algorithm-driven approach has resonated strongly with a broad spectrum of investors, driving a significant rise in adoption rates. This surge is fueled by their ability to offer cost-effective, transparent, and personalized financial advice, appealing particularly to tech-savvy millennials and retirees alike. Robo-advisors leverage data analytics and machine learning to maintain remarkably low error rates, continually refining their algorithms based on market trends and user preferences. This self-learning capability not only optimizes investment outcomes over time but also bolsters investor confidence in navigating dynamic markets, ensuring consistent returns, and solidifying their role in modern wealth management strategies. Benefits of AI-Powered Robo-Advisors Robo-advisors excel in managing data related to individual investor preferences, risk appetite, financial goals, and market trends. They gather and analyze data points such as income, age, investment horizon, and desired returns to recommend personalized investment strategies. These strategies typically include a broad range of investments including stocks, bonds, ETFs, and sometimes alternative assets like commodities or real estate investment trusts (REITs). Robo-advisors utilize algorithms to allocate and rebalance portfolios efficiently, aiming to optimize returns while adhering to the client’s risk profile. While they are proficient in data-driven decision-making, robo-advisors complement rather than replace human wealth managers. By handling routine tasks such as portfolio management and asset allocation, they free up wealth managers to focus on more complex financial planning and personalized client interactions. This symbiotic relationship enhances overall service delivery without jeopardizing the role of wealth managers, who continue to provide invaluable expertise and guidance in navigating complex financial landscapes. The Robo-Advisors market in India is projected to witness significant growth in the coming years. According to the Statista report, it is likely to grow at a projected annual growth rate of 9.21% between 2024-2027. Robo-advisors, like Niyogin’s own subsidiary platform InvestDirect https://www.moneyfront.in/ represent a disruptive force, democratizing access to personalized financial advice through AI algorithms. As AI evolves, they will play a pivotal role in shaping investment management’s future, offering personalized solutions catering to individual investors’ diverse needs and preferences. This competitive landscape will propel India’s economic growth, boost job creation, and position the Indian fintech industry as a strong contender in innovation and entrepreneurship.

How do neobanks appeal to young consumers in India?

Neobanks are ushering in a new era in banking by leveraging technology to provide modern, user-friendly services. In India, the technological revolution is particularly resonant with the younger generation. These digital natives are quick to embrace neobanks, drawn by their convenience, efficiency, and alignment with contemporary financial goals. Young consumers in the nation have quickly taken a liking to these cutting edge digital banks because these are not constrained by physical branches or antiquated systems. This blog examines the subtleties of their appeal and see how they align with the tastes and financial goals of the younger generation in India. Seamless Digital experience with innovative features Neobanks’ appeal stems from their ability to conform to the demands and expectations of the modern consumer. Customers of today are used to using their smartphones to plan every aspect of their daily lives, especially those belonging to the millennial and Generation Z generations. Neobanks provide digitally-first banking experiences in line with this trend, with features like instant account opening, real-time notifications, and access to individualized financial insights based on a person’s spending patterns and savings objective. Additionally, Neobanks are known for their inventiveness; they are always adding new services and features to meet the changing needs of their customer base. Digital-first banks provide a range of cutting-edge features that appeal to the tech-savvy generation, such as real-time payment notifications, customizable savings goals, and instant account opening with minimal documentation. Enhanced security and socially responsible banking Neo-banks usually place a high priority on security features like encryption, two-factor authentication, and real-time transaction tracking. By doing this, the chance of fraud or illegal access is decreased, and teenagers’ accounts and personal data are better protected. Young customers of today are more aware of environmental and social issues than ever before, and they want businesses they interact with to reflect similar values. A socially conscious approach to banking is frequently adopted by neobanks, which fund projects that advance community development, sustainability, and financial inclusion. Socially conscious millennials and Gen Z find great resonance in this dedication to social impact. Financial guidance and education A few neo-banks offer tools, resources, and advice that leverage advanced analytics and AI-driven algorithms to help teens form sound financial practices. They equip young consumers with features like spending classification, savings goals, and budgeting insights. Many neobanks go the extra mile to educate and empower their users through blogs, tutorials, and interactive tools to provide valuable insights into budgeting, saving, investing, and managing debt. By fostering a culture of financial awareness, neobanks help young consumers make informed decisions and achieve their financial goals. Neo-banks also come with tools that let parents or guardians monitor and manage their adolescent children’s accounts. This can help promote responsible financial behavior by letting them set spending limits, get transaction alerts, and keep an eye on their money. The path forward Looking ahead, the roadmap for neobanks in India includes expanding their user base and integrating more advanced financial services. Globally, neobanks have seen significant penetration, with over 20 million users in Europe and North America alone. In India, the market is burgeoning, with neobanks expected to reach 10% of the banking market by 2025, according to a report by Boston Consulting Group. With the government’s push towards a digital economy and increasing smartphone penetration, neobanks are well-positioned to revolutionize banking for the younger generation in India.

What is embedded finance and how does it benefit the fintech industry?

Embedded finance revolutionizes traditional banking by seamlessly integrating financial services into everyday non-financial activities, products, and interactions. This forward-thinking approach democratizes financial access, embedding services directly into consumers’ daily routines. By integrating banking, payments, lending, and insurance functions into sectors like e-commerce, retail, and mobility, embedded finance streamlines operations, enhances convenience, and elevates user experiences. This trend presents the fintech industry with a lucrative opportunity to broaden its horizons, reaching new customer segments and fostering innovation through the established infrastructure and user engagement of non-financial platforms. With embedded finance gaining traction, it promises to redefine how individuals engage with financial services, fostering a more inclusive and accessible financial landscape. How Embedded Finance Works Primarily, embedded finance integrates financial products and services into platforms directly through Application Programming Interfaces (APIs) and joint ventures between fintech companies, technology companies, and other enterprises. For instance, ride-hailing apps like Uber and Ola might allow users to conveniently pay for their rides with a digital wallet or bank account that is connected to these apps. Likewise, buyers may be able to obtain immediate financing or installment payment plans through e-commerce platforms at the point of sale, eliminating the need to go to a different banking website or app. Its Benefits for the Fintech Industry Embedded finance gives greater access to financial services by expanding the financial products and services market by integrating them into non-financial platforms. This financial democratization increases financial inclusion and gives marginalized groups access to necessary lending, payment, and banking services. A survey conducted by Accenture found that 76% of consumers are interested in using financial services offered by non-bank providers, highlighting the growing demand for embedded finance solutions. Also, by integrating financial services directly into their current platforms, embedded finance helps companies provide a smooth and frictionless consumer experience. This facilitates a more convenient and satisfied user experience by streamlining the user journey and lowering transactional friction. Research by Deloitte suggests that embedding financial services into non-financial platforms could increase customer lifetime value by up to 30% for businesses across various industries. Growth Trends The growth potential of embedded finance is immense, driven by technological advancements and shifting consumer preferences towards digital-first experiences. According to a report by McKinsey, the global embedded finance market is projected to reach USD 7 trillion by 2030. As more industries embrace digital transformation, the demand for embedded financial services is expected to rise exponentially. Startups and established fintech players alike are increasingly focusing on embedding financial capabilities into their platforms, expanding their service offerings and capturing new revenue streams. Overall, embedded finance presents an enormous opportunity for innovation, cooperation, and expansion in the fintech space. Businesses will expand access to financial services, improve customer experiences, and generate more value for industry stakeholders and consumers by integrating financial services into non-financial platforms seamlessly. Fintech businesses that adopt this paradigm shift and keep an eye on the embedded finance ecosystem could gain a competitive advantage and help mold the financial landscape of the digital era.

Technology’s revolutionary power in accelerating financial inclusion in India

Technology has emerged as a transformative force in reshaping India’s financial landscape, particularly in the realm of inclusion. Its revolutionary impact has been profound, breaking down traditional barriers and extending financial services to previously underserved segments of society. This evolution not only fosters economic empowerment but also strengthens the foundation for sustainable development. By leveraging technological advancements, India is witnessing a paradigm shift towards greater financial inclusion, ensuring that all citizens have equitable access to essential financial services and opportunities. Technology as a driving force for financial inclusion India has a fintech adoption rate of 87 percent, which is significantly higher than the global average and illustrates how technology has transformed the financial landscape of the nation. Through the use of mobile banking, digital payment systems, and other fintech innovations, financial services are now more easily accessible and reasonably priced, which lowers transaction costs. The public digital infrastructure facilitated by UIDAI has streamlined the digital shift, enhancing access to online banking services through groundbreaking advancements in identity verification and Know Your Customer (KYC) processes. Complementary efforts such as the Pradhan Mantri Jan Dhan Yojana and the India Stack have notably advanced financial inclusion and fostered fintech adoption in India. These initiatives have not only facilitated the emergence of innovative tech products by fintech startups but have also laid a solid digital groundwork to support both public and private digital endeavors. Especially noteworthy is the substantial benefit extended to marginalized communities. The widespread availability of mobile banking services has sparked a transformative change in rural areas, granting underserved populations convenient access to online banking and credit facilities. This expansion has effectively bridged the rural-urban gap, fueling economic development and mitigating income inequalities. Moreover, it has facilitated easier access to credit services for micro, small, and medium enterprises, thus contributing to the overall growth of the economy. Fostering Equality Through Technological Advancements In the fintech realm, various risks, including cybersecurity threats, regulatory complexities, data privacy concerns, disparities in digital literacy, and issues with customer trust, pose challenges. To sustain growth, all stakeholders must address these challenges thoughtfully while encouraging innovation. Continuous investment in Digital Public Infrastructure (DPI) is crucial to establish a resilient digital environment for fintech transactions and to ensure fair competition. Countries such as Singapore and India have already demonstrated success in deploying DPI through collaborative efforts between the public and private sectors. Another noteworthy development is the recent approval of the First Loss Default Guarantee (FLDG), which underscores the effectiveness of the bank-fintech partnership model in digital lending. With a global count exceeding 400 million, MSMEs underscore the pivotal role of technology in transformation. Technology has revolutionized the way millions of Indians access and manage their finances, speeding up the process of financial inclusion. Even with the tremendous advancements, continued work is essential to improve infrastructure, cybersecurity, and digital literacy. Taking care of these issues will allow India to enhance its ongoing efforts to promote innovation and partnership among stakeholders, paving the way for a more accessible and prosperous future through initiatives aimed at enhancing financial inclusion.

The future of money: Gearing up for Central Bank Digital Currency