Approximately 1.5 billion individuals globally lack access to banking or comparable financial services. For the rest of us, less than half of those with bank accounts are eligible for lending. More intelligent credit assessment methods are needed to increase banks’ loan-making capacity. Thus, AI-driven credit scoring models have emerged as a game changer, providing more accurate, efficient, and equitable means of evaluating credit risk.

- Traditional Credit Scoring Restrictions: Traditional credit scoring models have been in use for decades and primarily rely on a few key characteristics, such as a person’s credit history, payment history, outstanding debt, duration of credit history, and credit types used. While these models have fulfilled their purpose admirably, they are not without limits.

- Lack of Comprehensive Data: Traditional models frequently rely entirely on credit bureau data, which might exclude several important elements that may influence creditworthiness, such as income, employment history, and savings.

- Inflexibility: Traditional models are relatively inflexible and cannot adjust to changing economic conditions or individual circumstances. They have predefined thresholds that may not account for complex credit risk evaluations.

The Importance of AI in Credit Scoring

Machine learning algorithms are used in AI-powered credit scoring to overcome the limitations of traditional models and provide a more holistic and accurate credit risk assessment. Here’s how AI will impact credit scores in the coming times:

- Expanded Data Sources: AI models take into account a diverse set of data sources, such as bank transactions, social media profiles, and other non-traditional information. This additional information contributes to a more complete picture of a borrower’s financial health.

- Dynamic Scoring: AI models can adjust to shifting financial situations and economic elements in real time. This flexibility is especially useful during economic downturns or for borrowers with shifting incomes.

- Reduced Bias: AI algorithms are supposed to be more unbiased, eliminating human biases that can enter into traditional scoring techniques. They hold the promise of more equitable financing decisions.

- Improved Accuracy: Because AI algorithms can analyze massive volumes of data, they can provide a more accurate assessment of a person’s creditworthiness. This allows lenders to make better-informed lending decisions, lowering the chance of default.

- Faster Decision-Making: With AI, credit scoring can be done in real time, greatly accelerating the loan approval process. Borrowers have faster access to funds, which is especially crucial for personal and small company loans.

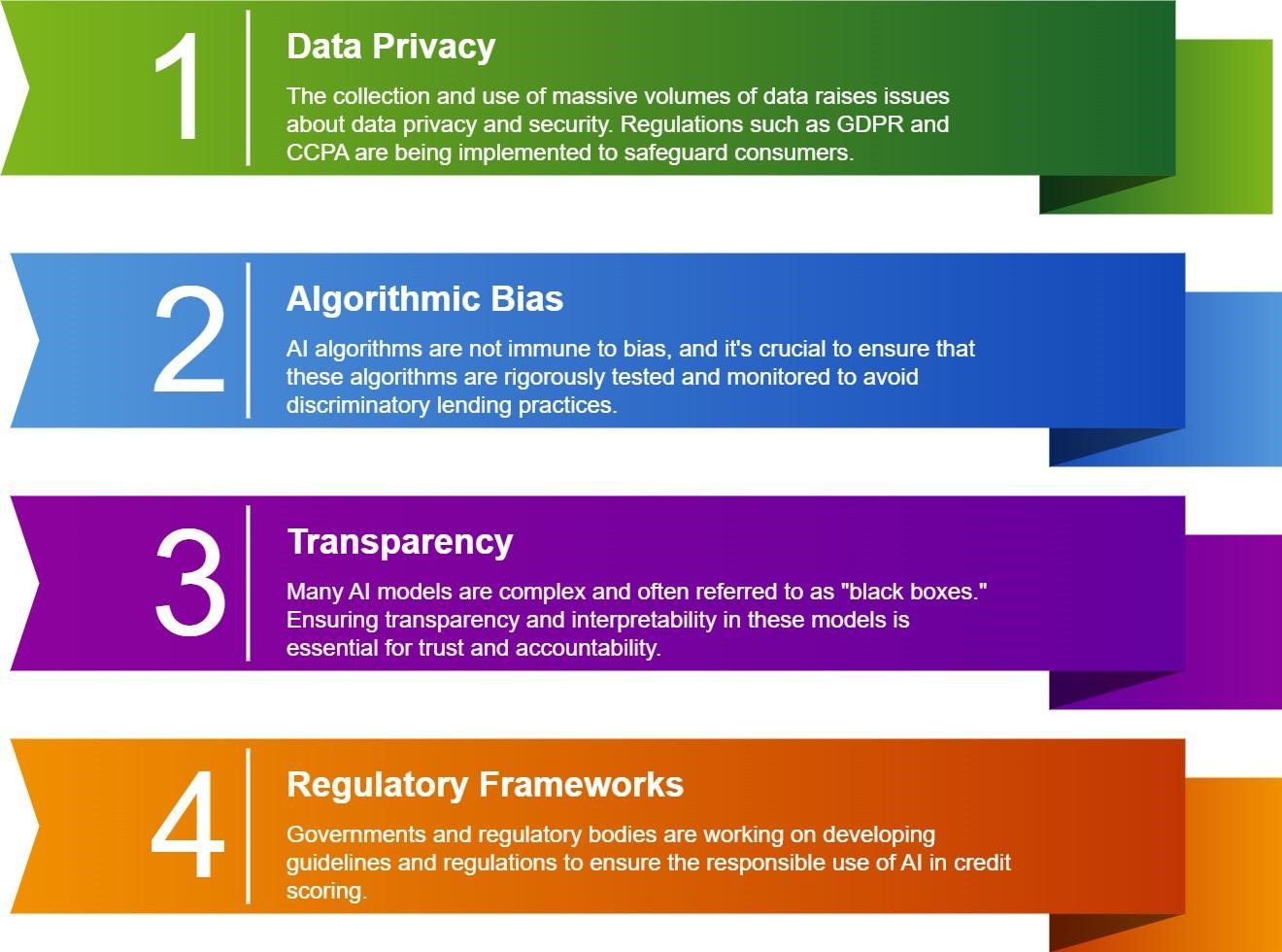

While artificial intelligence has made significant breakthroughs in credit rating, there are still issues and concerns that must be addressed.

To summarize, AI is playing a transformative role in the world of credit scoring. However, in order to reap the benefits of AI ethically, the financial industry must address issues such as data privacy, bias, transparency, and regulatory compliance. As technology advances, the importance of AI in credit assessment is expected to grow even more, suggesting a future in which lending decisions are more inclusive, accurate, and rapid.