The digital revolution has irrevocably reshaped industries worldwide, and the credit sector is no exception. Technological advancements are propelling a paradigm shift in how individuals and businesses access financial resources. With unprecedented speed, convenience, and inclusivity, digital platforms are democratizing credit, making it more accessible to a broader range of borrowers. Expanded Access to Credit One of the most significant impacts of digital platforms is the expansion of credit access. Traditionally, obtaining credit often required navigating cumbersome paperwork and dealing with lengthy approval processes. Digital platforms, however, streamline these processes, allowing users to apply for and receive credit with just a few clicks. According to a 2023 report by the World Bank, digital lending platforms have increased credit access by 20% in emerging markets, where traditional banking infrastructure is often limited. Enhanced Inclusivity Digital platforms are also breaking down barriers to credit for underserved populations. Fintech companies leverage alternative data—such as payment histories from utilities and telecommunications—to assess creditworthiness, making it easier for individuals without traditional credit histories to access loans. This approach has proven effective; a study by the McKinsey Global Institute found that alternative data usage in credit scoring has led to a 25% increase in loan approvals for individuals from low-income backgrounds. Efficiency and Speed The efficiency and speed of digital credit platforms surpass traditional methods. Automated systems and artificial intelligence (AI) allow for rapid processing of applications and real-time credit scoring. A recent survey by PwC revealed that 65% of borrowers on digital lending platforms reported receiving their funds within 24 hours of application approval, compared to an average of 10-15 business days through traditional banks. This rapid turnaround is particularly beneficial for small businesses and individuals facing urgent financial needs. Personalization and Customer Experience Digital platforms enhance the borrower experience through personalized services. AI-driven algorithms analyze user behavior and preferences to offer tailored credit products and recommendations. This personalization improves user satisfaction and helps borrowers find products that best suit their needs. According to a report by Accenture, 70% of users on digital lending platforms reported higher satisfaction levels due to the personalized nature of the services they received. Data Security and Privacy Despite these advancements, digital platforms must address concerns around data security and privacy. With the increased reliance on personal and financial data, safeguarding this information becomes crucial. Leading platforms invest in advanced encryption technologies and adhere to stringent regulatory standards to protect user data. For instance, the European Union’s General Data Protection Regulation (GDPR) has set a high standard for data privacy, and compliance with such regulations is becoming a norm for global digital credit platforms. Future Outlook Looking ahead, digital platforms are expected to continue driving innovation in credit access. Advances in technologies such as blockchain and biometric authentication promise to further enhance security and streamline processes. As digital platforms evolve, they will likely offer even more inclusive and efficient solutions, making credit accessible to an increasingly broad audience.

Tag: credit

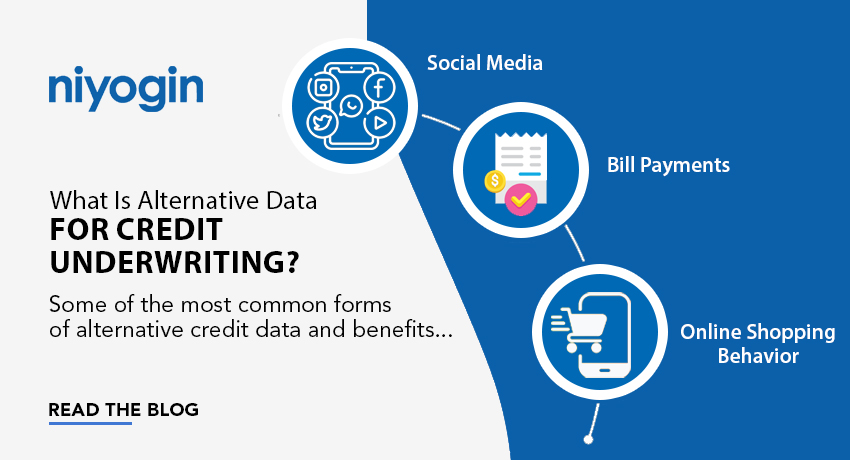

What Is Alternative Data for Credit Underwriting, and How Your Lenders Gain Access to It?

Banks, NBFCs, and other financial organizations in the lending business use credit underwriting to assess a borrower’s risk profile. However, using alternative data to evaluate creditworthiness can greatly improve credit assessment accuracy, especially for individuals and enterprises with limited or unusual credit histories. Alternative credit underwriting data refers to information not typically used in the traditional credit underwriting process. This can include data from rental payments, telecom and mobile data, online shopping behavior, utility payments, social media activity, public records, etc. The use of alternative data in credit underwriting is becoming increasingly popular as lenders look for new ways to assess the creditworthiness of potential borrowers. This is known as alternative credit data, which can include information from various sources beyond the traditional credit bureaus. Some of the most common forms of alternative credit data used by lenders include: Alternative Financial Services Data This data includes information on consumers’ use of small installment loans, single-payment loans, point-of-sale financing, auto title loans, and rent-to-own agreements. It can provide information about a consumer’s payment history and creditworthiness. Consumer Permission Data With a consumer’s agreement, lenders can access transactional and account-level data from financial accounts to better estimate income, assets, and cash flow. This information can also provide insight into payment history on non-traditional accounts such as utilities, cell phones, and streaming services. Rental Payment History Property managers, electronic rent payment providers, and rent collection firms can all share information about consumers’ rent payment history and lease terms. Full-File Public Records Public records at the local and state levels can provide information on a consumer’s professional and occupational licenses, education, property deeds, and address history. Data on Buy Now, Pay Later (BNPL) Payment and return history, as well as upcoming planned payments, can be displayed in BNPL trade line and account data. This information can provide insight into a consumer’s creditworthiness, which may become even more relevant as consumers increasingly use this new sort of point-of-sale financing. Benefits of Using Alternative Data The use of alternative data provides a more holistic view of a borrower’s financial situation and helps lenders make more informed decisions. Alternative data helps lenders reach a wider pool of potential borrowers. Alternative data can be handy for borrowers with limited credit history or credit problems in the past. The use of alternative data helps lenders reduce fraud and risk. Alternative data can be used to verify the information provided by borrowers. With the use of alternative data, lenders can assess a borrower’s creditworthiness more efficiently and cost-effectively. Lenders can use alternative data to offer personalized loan products to borrowers. Alternative data can be used to identify new market segments and opportunities for lending. Alternative data helps lenders stay competitive in a rapidly changing lending environment. Gaining Access to Alternative Data Through partnerships with data providers These lenders collect and analyze data from various sources, including social media accounts, mobile phone usage, and online shopping behaviour. They then package this data and sell it to lenders, who can use it to make more informed lending decisions. By using specialized software that extracts data from online sources This specialized software can collect data from various sources, including social media accounts, mobile phone usage, and online shopping behaviour. Lenders can then use this data to assess the creditworthiness of potential borrowers. Lenders may use customer-permission data. Some customers agree to share data with the lender to improve their creditworthiness. For example, a customer may give a lender permission to access their online banking information, which can provide insight into the customer’s spending habits and income. This data can be used to make more informed lending decisions. As technology advances, we should expect to see more alternative data sources employed in credit underwriting. However, lenders must carefully weigh the dangers and benefits of using alternative data and guarantee that it is used ethically and responsibly.

Alternative Finance Instruments: How Do They Help SMEs Grow?

Alternate financing describes a category of financing products that includes venture capital, invoice finance, cash flow loans, and debts. In India, such solutions are now primarily favoured by SMEs and startups. This pattern is a component of the broader drive towards financial inclusion, which aims to increase access to formal banking institutions for more individuals. According to the World Bank, financial inclusion is ensuring that companies have access to practical, reasonably priced financial solutions that satisfy their needs in an ethical and sustainable manner.India accounts for around 81.3% of the South Asian market. By 2030, digital lending in India is estimated to reach $1.3 trillion. Artificial intelligence is used by digital lenders to analyze creditworthiness, allowing these fintech firms to reach underserved populations. National digitization activities also contribute to the expansion of alternative financing. The Rise of Alternative Financing Start-ups and SMEs must adapt to the increased requirement for remote working as a result of the pandemic. Due to the requirement for scaling, SMEs sought alternative funding sources. With the advancement of technology and the advent of artificial intelligence, organizations continually require financial resources to compete in today’s market. This growth in innovation has always resulted in a diversity of finance strategies to assist SMEs. Alternative financing solutions for small enterprises include peer-to-peer lending, cash flow, crowdsourcing, and invoice financing. Alternative Financing Drives SME Growth SMEs that have been denied funding from traditional loan providers such as banks and financial markets look to alternative financing sources to obtain the capital they want. In developing nations such as India, it is estimated that over 83% of SMEs lack appropriate finance. The growth of the fintech industry has prompted SMEs to invest in fintech services and seek other forms of financing. The emergence of fintech and alternative finance models has resulted in a faster loan approval procedure, the acceptance of smaller loans, and a reduction in the cost of capital and transactions for SMEs. Fintech has played a significant role in increasing the number of investors due to its diverse financing structures and growing array of investment methods. Peer-to-peer lending has gained popularity, aided by fintech websites. Interested investors can use P2P platforms to connect with borrowers looking for loans, eliminating the need for a financial institution. Competition from the peer-to-peer sector will also motivate banks to use fintech services to provide financial support to SMEs. As of March 2022, the lending market in India rose by 11.1% This expansion is due to the lending sector’s shift towards alternative finance, which is aided by data-driven lending. As a result, SMEs and small firms are no longer restricted to the traditional bank loaning structure due to the availability of alternative financing options. In this modern age of growing fintech services and AI models, the funding system has been positively impacted as it has attracted a large number of new investors who would not have been players in the market if not for the variety of different investments and return on investment options.

How is Fintech Revolutionizing Credit Scores?

The fintech revolution has impacted the financial industry in a variety of ways, with credit scoring being one of the most disruptive. Credit scores have traditionally been established using restricted data, frequently omitting people with little or no credit history. However, with the rise of fintech, forward-thinking businesses are using technology, alternative data sources, and advanced analytics to revolutionize credit ratings. Image Source: Google Fintech changing credit scores and its benefits to consumers and lenders Increasing Data Sources Fintech firms are leveraging the power of technology to access data sources other than traditional credit agencies. Fintech firms may provide a more comprehensive image of an individual’s creditworthiness by examining a broader range of data, such as utility bills, rent payments, and even social media activity. As a result, they can now measure creditworthiness for people who were previously underserved by the standard credit scoring paradigm. Inclusion of unbanked and underbanked individuals One of the primary benefits of fintech-driven credit scoring is its capacity to include people who are unbanked or underbanked. These people may have limited access to standard financial services and no official credit history. Fintech firms can use alternative data and creative scoring models to assess creditworthiness based on criteria such as income, savings patterns, and transaction history. This inclusion gives underprivileged people access to credit and financial services that were previously unavailable to them. Improved Accuracy and Risk Assessment Fintech’s data-driven approach to credit scoring improves risk assessment accuracy. Traditional credit ratings frequently focus mainly on payment history, ignoring important aspects like income, education, and employment history. These extra data points can be incorporated into fintech models to create a more comprehensive assessment of an individual’s creditworthiness. This enables lenders to make better-informed decisions and provide personalized lending packages customized to the specific demands and circumstances of each borrower. Speed and Efficiency Fintech firms use innovative technologies and automation to streamline the credit evaluation process. They can analyze vast amounts of data quickly and deliver near-instant credit judgements by utilizing algorithms and machine learning. This speed and efficiency benefit both lenders and borrowers by lowering the time and effort required to acquire credit while reducing the danger of human error. Facilitating Financial Inclusion The significance of fintech-driven credit scoring in fostering financial inclusion is one of its most important achievements. Fintech companies are breaking down barriers and boosting access to finance for previously underrepresented populations by leveraging alternative data sources and advanced analytics. Individuals will be able to establish credit, get inexpensive loans, and engage more fully in the economy as a result of this inclusion, leading to increased financial empowerment and economic prosperity. Fintech is transforming credit ratings through the use of technology, alternative data sources, and advanced analytics. This game-changing strategy broadens the pool of people who can obtain credit, empowers the unbanked and underbanked, and improves the accuracy and efficiency of credit evaluation. Financial inclusion is being promoted through fintech-based credit scoring, which ensures that more people have access to affordable loans and financial services. The credit scoring landscape will continue to alter as the fintech revolution proceeds, empowering individuals and transforming the way creditworthiness is assessed.

The Rise of Digital Identity Verification in Fintech Credit

Digital identity verification has evolved as an important component of credit evaluation processes in the fast-paced world of financial technology (fintech). Traditional methods of verifying identities for credit applications, such as manual document checks and in-person verification, are time-consuming, error-prone, and out of step with today’s customer expectations. Fintech firms are utilizing cutting-edge technologies and digital solutions to revolutionize identity verification, thereby improving security, efficiency, and customer experience. What is Digital Identity Verification? A digital identification service is a process that allows consumers to securely access their financial and legal information. We can easily communicate and protect our personal and sensitive information by using identity verification services. Advantages of Digital ID in Fintech and Online Banking Exceptional Customer Service Customers benefit from a seamless experience since digital identification verification simplifies and streamlines the credit application procedure. Fintech companies may verify identities in seconds by leveraging technology like face recognition, biometrics, and artificial intelligence (AI), eliminating the need for clients to provide physical documents or visit a physical location. This frictionless experience improves client happiness and increases credit application conversion rates. Improved Security and Fraud Prevention Digital identity verification improves security and reduces the danger of identity theft and fraud. Fintech companies can use advanced technologies to validate identification documents, identify tampering or forgery attempts, and undertake liveness checks to guarantee the person presenting the identity is physically present. These strong security measures safeguard both customers and lenders, lowering the likelihood of fraudulent activity in the credit ecosystem. Access to Previously Untapped Markets Credit availability to traditionally underserved populations, such as the unbanked and underbanked, could be expanded with digital identity verification. Traditional credit assessments frequently rely on traditional credit bureau data, which excludes people who do not have a formal credit history. Fintech organizations can assess creditworthiness based on characteristics such as payment history, income, and transaction patterns by leveraging alternative data sources and advanced analytics. This inclusion helps underserved people obtain credit and establish financial profiles, thereby promoting financial inclusion and economic empowerment. Regulatory Compliance Fintech firms operate in a highly regulated environment, and adhering to Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements is critical. Digital identity verification systems assist in satisfying these compliance standards by automating identity checks, certifying document authenticity, and completing risk assessments. These digital solutions ensure that fintech organizations meet regulatory requirements, lowering compliance risks and increasing operational efficiency. Scalability and Cost effectiveness Manual identity verification techniques are time-consuming, labour-intensive, and not scalable. To handle increasing numbers of credit applications, fintech organizations require nimble and efficient solutions. By automating the verification process and eliminating the need for manual involvement, digital identity verification provides scalability and cost effectiveness. Because of this scalability, fintech firms can manage a larger volume of credit applications while keeping expenses under control. Steps to Create a Trusted Digital Identity: – Digital identity verification is altering the financial credit market by providing a transformational approach to identity verification. Fintech firms are improving consumer experiences, tightening security measures, expanding loan access, maintaining regulatory compliance, and improving operational efficiency by employing sophisticated technologies. The rise of digital identity verification is changing the way credit applications are processed, decreasing friction, increasing security, and promoting financial inclusion. As the fintech sector evolves, digital identity verification will remain a critical component in offering seamless and secure credit experiences for individuals and organizations alike.

Financial Inclusion; the need and future

Financial inclusion refers to the process of ensuring access to affordable financial services, such as banking, insurance and credit, to all sections of society, particularly the underprivileged and low-income groups. Data Points to understand Financial Inclusion The need for Financial Inclusion Addressing poverty – Financial inclusion can help to alleviate poverty by providing access to formal financial services and promoting savings and investment habits among low-income households. Currently, India faces poverty in 75% of rural and 50% of urban households, totaling an official poverty percentage of 62.5%. Addressing the basic financial needs of the said population is the need of the hour to ensure we boost financial inclusion. Promoting economic growth – Financial inclusion can contribute to economic growth by enabling the flow of credit to small and medium-sized businesses, which are often the backbone of the Indian economy. With MSMEs contributing over 30% of the GDP, it is a pressing priority to assist them financially. Reducing income inequality – Financial inclusion can reduce income inequality by providing financial services to underserved sections of society, including rural areas and women. As per data, the pandemic has led to a further contraction of income and wealth in the bottom 50% of India. The top 30% own 90% of India’s wealth and interestingly, the top 10% own over 72% of India’s total wealth and the top 5% of the population owns nearly 62% of the wealth. Understanding the statistics makes us realize the staggering disparity in income. As per the Reserve Bank of India, only 27% of Indian adults are financially literate. This makes it easier for intermediaries and informal financial systems to defraud the illiterates. However, with educational programs, this issue can be addressed and eliminated. Promoting financial stability – Financial inclusion can help to promote financial stability by reducing the reliance on informal and unregulated financial systems that are often associated with fraud and other illegal activities. Empowering individuals – Financial inclusion can empower individuals by enabling them to make informed financial decisions, access credit, and invest in their future. The future of Financial Inclusion The future of financial inclusion in India looks promising, with significant progress made in recent years. Putting digital transformation at the forefront by the government and financial institutions has accelerated and is further expected to accelerate inclusivity in the coming years. With MSMEs and underserved individuals steadily adopting internet banking, mobile banking, etc., a digital shift can be expected. With Fintechs and NBFCs joining strengths, the collaboration has been beneficial for the financial domain. Better innovation with robust financial products and services that cater to the specific needs of the underserved has been introduced and executed in the market. This customization and personalization only seem to get better with time and adaption. However, it is important to note that financial literacy plays a very critical role in everything we have spoken of thus far. Without basic awareness and literacy to make informed decisions, every other initiative may prove futile. The government, along with several initiatives, has joined forces with financial institutions to convey awareness and literacy to the last mile. In conclusion, the future of financial inclusion in India looks promising, with the potential to improve the lives of 900 million people by providing access to formal financial services, promoting savings and investment, and reducing poverty and inequality.

What Is Credit Risk Evaluation?

The retail loan industry in India is growing rapidly. Compared to March 2021, the retail loans increased by 50% in March 2022. NBFCs are mainly responsible for this huge surge in the growth of personal lending. Issuing credit cards also grew by 13%. Lenders are more willing to increase loans and credits mainly because of the change in the credit underwriting process. From March 2021 to March 2022, ₹24 crore loan was disbursed. Traditionally, credit limit evaluation is a manual process. People looked at income slips, loan repayment receipts, and other documents to evaluate the credit limit of a person. This type of evaluation was heavily biased and based on the individual’s perception of lending. For example, two businesses in Delhi and Jabalpur would not get the same credit limit even if their income and financial status is the same. Geographical locations too played a critical role in credit limit because someone from Delhi will get a higher credit limit than someone from Jabalpur. Modern and technology-based credit evaluation approach takes the guesswork out of the process. Standardized metrics are used and numerous different financial parameters are considered for approving credit limits. Now, people in second-tier cities will also have access to higher credit limits, irrespective of where they are located. Fintech companies use advanced automated APIs to evaluate creditworthiness solely based on financial status. This has allowed financial institutions to offer loans symmetrically throughout. Credit Risk Evaluation Benefits For Banks Credit risk evaluation models that rely on historical data are inaccurate and outdated. Improved and streamlined evaluation models are the need of the hour for banks and NBFCs that are competing to improve loan offerings. Automated evaluation models can predict customer behaviors and tap into new data sources. It opens up new market segments, increasing the reach of financial institutions. Revenue increase – When the new dynamic model of credit underwriting is employed, data from multiple sources are fetched to calculate creditworthiness. Based on new models, banks can increase their revenue by 5% to 15%. This is possible by lowering the cost of acquisition, increasing acceptance rates, and offering a good customer experience. Reduce credit-loss rates – If the evaluation model can predict and pick out customers more likely to default, banks can reduce their credit losses by 20% to 40%. This can greatly help banks to improve their capital and diversity service offerings. Improved efficiency – Automated data extraction, evaluation ML models, and case prioritisation can improve banking efficiency by 20% to 40%. Low-risk cases can be processed quickly. High-risk cases are analyzed more thoroughly based on improved evaluation models. How To Implement New-Age Credit Evaluation Models? Fintech in the banking sector involves automating banking processes to create an agile environment. The best way to develop a credit evaluation model is to expand data sources and mine existing data to find credit signals. Use A Modular Architecture Credit risk evaluation varies on a case-by-case basis. Hierarchical architecture is not suitable anymore. Modular architecture for credit risk evaluation models allows fintech companies to add or remove data sources based on the creditor risk. Using this model, banks can gather financial information from multiple data sources and assign scores based on the importance of data to evaluate creditworthiness. Gather Data From Multiple Data Sources The decision-making model should have a predictive analysis capacity to evaluate credit risk. The future risk of a creditor can be evaluated using historical data. Apart from traditional data, use non-traditional and external data for underwriting. Use Data Mining To Identify Credit Signals While the data sources are useful, the true potential of credit risk evaluation models can only be unlocked with proper data mining tools. Data from multiple sources must be pulled together, compared and analysed to identify credit signals. Modern-day ML models can take incomplete or partial banking data and predict the customers’ outlook for categorisation. This helps in segmentation based on geographical location, past financial history, etc. Leverage Fintech Expertise While credit risk evaluation is crucial, NBFCs need not spend their resources building a brand-new credit risk evaluation model. They can leverage the technical and cloud expertise of fintech partners to build upon the evaluation model they already have. As the new models are modular, banks can determine the type of evaluation modules necessary based on the target market.

Introducing Supply Chain Finance

Supply Chain Finance (SCF) is a technology solution that lowers financing costs for buyers and sellers. It tracks invoice approval and settlement and automates transactions to improve the efficiency of all the parties involved in a sales transaction. The supply chain financing market is expected to reach a CAGR of 17.1% by 2024. According to Mckinsey reports, SCF eligibility will increase from less than 40% to as much as 80% in the upcoming years as supply chain leaders are looking for better solutions. By 2031, the supply chain finance market is expected to reach $13.4 billion. Indian Supply Chain Financing Ecosystem Challenges Compared to global trends, India’s supply chain financing (SCF) is still nascent. Indian MSMEs employ more than 11 crore people and contribute 29% of the GDP. Also, 70% of MSMEs require working capital funds. However, SCF remains inaccessible due to the legacy banking systems. Many MSMEs don’t meet the banking requirements criteria. The estimated credit gap is Rs. 20-25 trillion. This credit gap forces the MSMEs to approach third-party lenders, which results in higher costs, stunted growth, low profitability, and a volatile business model. The COVID economic disruption doesn’t help either. The low-cost SCF option provides extended financing for MSMEs and helps lenders manage credit risks. Source: Allied Market Research According to the new Factoring Regulations Act 2011, more than 182 NBFCs can now offer factoring services. Previously, NBFCs could meet only 20% of the funding requirements for MSMEs. Digitisation Is Paramount To SCF Innovation Digitisation is the key to achieving seamless SCF solutions for Indian MSMEs. Businesses will have access to more customised SCF products that help increase the working capital. Apart from invoices, businesses can benefit from other fintech offerings such as a letter of credit, import and import bills, shipping guarantees, performance bonds, and more. Technology innovations such as fintech digital delivery, industry utilities, API technologies, and blockchain bring supply chain financing closer to SMEs. With the non-availability of credit history, lenders can use AI-based risk assessment solutions to evaluate creditworthiness. Such solutions also predict business growth, enabling lenders to offer SCF financing. Source: PWC Fintechs can bring about innovation in SCF solutions in the following ways: Incorporate API-enabled services using a customer-centric tech stack. Use data to understand supply chain networks to innovate new opportunities. Use blockchain-distributed ledgers to improve the transparency of the financing platform. Introduce innovative products such as CAPEX discounting, invoice discounting, warehouse receipt finance, dynamic discounting, early cycle discounting, and SCF securitisation. Various initiatives from the Government of India encourage SCF. The fintech platforms can use the existing rails to improve their SCF offerings in the following ways: Leverage TReDS and GSTN linking to understand MSME cash flows for invoice financing better. Use the AA framework to provide financing options for suppliers and buyers. India’s addressable supply chain market is estimated to be Rs. 60,000 crores, while the total market value is Rs. 18 lakh crore. Digital supply chain solutions facilitate fully trackable transactions to seamless trading between buyers and suppliers.

Lending as a feature in the future

Lending has been a fundamental mean of money circulation in the economy. Over the years, we have seen a remarkable shift in how lending is undertaken. The shift from physical to phygital to digital has been massive and we are still evolving! In the past, lending was an independent process that had rigid prerequisites. Owing to technology, the approach has transformed and at present, financial institutions are devising ways to disburse loans within minutes. What created value in the past? The past two decades of value creation in the lending business has been through a focussed execution of time tested formula of raising Current Account Savings Account (CASA). Traditional banks focused on individuals with the capacity to deposit money with them thereby creating value. This deposited money is then circulated in the market as ‘loans’. In the individual lending area, customers plan their purchase and then hunt for the right lender to borrow yet, retail lending, through the cycles, has been the biggest value driver for banks in the lending business. However, this approach is set to change in the next decade or even earlier. For instance, Buy Now Pay Later (BNPL) is changing how customers function. Financial institutions are offering immediate credit to individuals transforming the entire ‘plan your purchase’ notion. Why is it going to change? Customer engagement- Customers view banking tasks as a standalone activity and use banking facilities for specific tasks. Not all banking activities are embedded in the transaction flow and this is likely to change in the coming future. Customer experience- Banks have largely replicated branch processes into digital workflow with no real change in the first design principles of banking service delivery. With upstarts emphasizing on customer journey, customer experience will be heavily emphasized upon. Data- Banks possess legacy transaction and customer data making them work on stale financials. This approach is likely to transform with a change in workflow owing to technology, innovation and customer demand. Asset Quality- With better positioned platforms to judge capability, banks have the intent to innovate and will eventually indulge in the following to transform- Banks do not have dynamic propriety transaction data and democratisation of access to static data with account aggregators and OCEN can help banks maintain asset quality. Platforms that are used by customers are not only to offer better CX but will also be in a better position to judge capability with bank’s own transaction data. Platforms will be able to feed the credit to drive purchases and transaction on their own program. What will be the impact of emergence of new business models? With emergence of fully integrated financial services model of manufacturing (banks), digital platform and customer acquisition will be unsustainable with rising CACs and no differentiated value proposition from banks. Business models will segregate and specialize into manufacturing (banks), platform infrastructure and customer front ends. For instance, Zomato, Udaan, Amazon etc. have already integrated and offer an end to end platform. The opportunities associated specifically with business models are- While platforms and customer front ends are quickly moving to adopt lending as a feature, regulatory guidelines and the obsession with leading current manufacturers (banks) is leading to almost no players constructing this. Platform (API) Infrastructure players enabling any/all companies to offer financial services products The likely outcome – Lending to become a product ‘feature’ With infrastructure development, customer ownership and engagement is shifting to platforms. Retail Lending will be embedded in the transaction flow. Every tech platform with customers/sellers will offer lending as a ‘feature’. Reasonably priced embedded credit at the time of transaction to be part of customer experience and product proposition. Conclusion Infrastructure plays a very critical role in the given scenarios and their achievement. Embedding ‘lending as a feature’ on all platforms will require a robust and secure infrastructure and platform wherein customers have a seamless CX.